Equity bulls marched into the trading week with a renewed sense of vigour after last Friday’s US jobs report smashed expectations.

Although several major markets were closed on Monday due to the Easter weekend, Asian stocks flashed green while the S&P 500 and Dow Jones surged to record closing highs.

On Tuesday, the mood across Asia was mixed amid fears around a new Covid-19 variant in Japan leading to a possible fourth wave. Europe finally caught up with Wall Street as traders returned from their desks after the Easter holiday break. In the currency markets, the Euro stood tall against its major counterparts while the Dollar stabilized near an almost two-week low…

Our Chief Market Strategist Hussein Sayed made an interesting comment on the divergence between US economic growth and the rest of the developed world, which may push the Dollar higher in Q2.

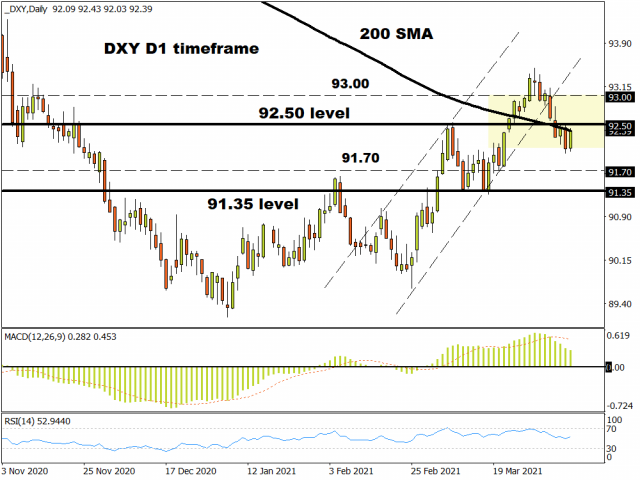

In our technical outlook, we covered the Dollar ahead of the Federal Reserve minutes on Wednesday evening. The Dollar Index (DXY) later tumbled to a fresh two-week low at 92.00 following the dovish Fed minutes. According to the minutes from the March meeting, officials expressed optimism about the economy’s prospects but remained cautious over the ongoing risks posed by Covid-19. Overall, the Federal Reserve seems to be in no rush to end its ultra-accommodative monetary support.

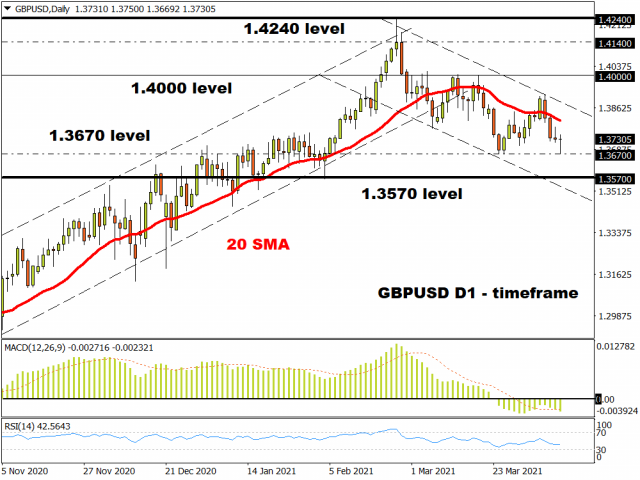

In other news, the British Pound was the worst-performing currency this week amid concerns over the UK’s vaccine rollout.

The currency has weakened roughly 0.7% against the Dollar, with prices trading around 1.3730 as of writing. Should the Pound extend losses in the week ahead, the GBPUSD may descend towards 1.3570.

Thursday was another day, another record high for indices across the globe as equity bulls welcomed the dovish Federal Reserve minutes. European and UK stocks set new records while the S&P 500 notched a fresh record close.

Speaking of indices, our Market Analyst Han Tan dissected this topic with Nasdaq on the Markets Extra podcast.

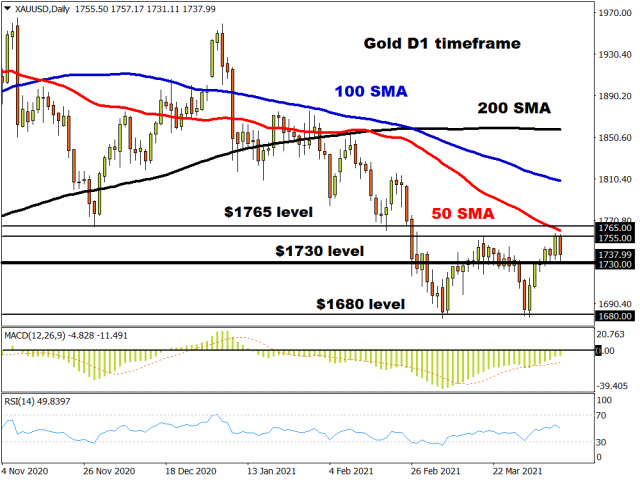

Looking at commodities, Gold has retreated from its highest level this month but remains on path for its first weekly gain in three. The precious metal remains supported by a softer Dollar, falling bond yields, and fresh dovish comments from Federal Reserve Jerome Powell.

In regards to oil, prices have shed over 3% this week as investors evaluated the rising supplies from major oil producers and possible impact on fuel demand from lockdown restrictions in Europe.

Overall, it has been a positive week for global equity markets. The MSCI ACWI index posted a new record high on Thursday. The million-dollar question is how much longer will the bull party last?

Fasten your seat belts and be prepared for potential volatility next week when the US earnings season kicks off. Keep an eye on the Covid-19 developments and lockdown restrictions across Europe. There will also be speeches from financial heavyweights and key economic data from major economies.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.